Just like with many new technologies, governments are notoriously slow on the uptake.

It has long been known that, unlike private organizations, governments typically have a difficult time weaving new technologies into their infrastructure, due to the number of regulatory hurdles, a typically low risk appetite, and intense scrutiny from the public.

But governments around the world are now looking to buck the trend, by using blockchain and related technologies to launch central banked digital currencies (CBDCs).

Adopting New Technology

Though disruptive technologies are appearing at an ever-faster rate, it can take years, or even decades before they are adopted by governments.

Blockchain is one of these disruptive technologies, since it allows data to be communicated completely securely across a public or private ledger, in a way that is both cheap and irreversible. This technology has mostly been adopted for a large number of public cryptocurrency projects, which allow holders to transfer value across borders, without worrying about censorship, high transaction or remittance fees, or fraud.

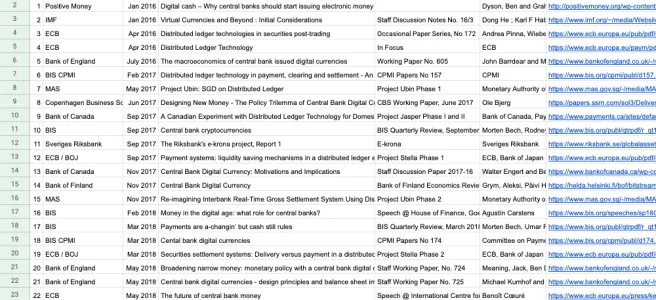

An overview of current CBDC projects. (Image: Antony Lewis)

But now, numerous governments around the world are beginning to experiment with their own take on cryptocurrencies—producing CBDCs. These are essentially digital versions of standard fiat money, such as the Chinese yuan (CNY), Pound sterling (GBP), and euro (EUR). Unlike open-source cryptocurrencies like Bitcoin and Ethereum, these CBDCs would be controlled by the central bank, who would control the issuance and distribution of CBDC units.

Overview of Current CBDC Projects

Although the prospect of a ready-to-launch CBDC is likely several years away at the very least, a large number of countries are already working on their implementation of the technology.

According to cryptocurrency exchange Remitano, around a dozen countries are currently piloting their CBDC, including Belarus, South Africa, Sweden, and Ukraine. Likewise, A 2019 report by the Bank For Initial Settlements (BIS) indicates around 70% of central banks are working on a CBDC project.

However, China is arguably the furthest ahead in the development of its digital fiat currency project, known as the Digital Currency Electronic Payment (DCEP).

News about China's CBDC project first appeared in 2019 and development appears to have moved on swiftly since then. Each DCEP unit is backed by the official currency of China, the Chinese yuan, the official currency of China.

But unlike many other CBDC projects, the DCEP doesn’t actually use a blockchain base. Instead, the central bank of China plans to use a blockchain-like system that enables peer to peer, tamperproof payments that can be settled almost instantly. Being backed by the CNY, conducting transactions using the DCEP is the equivalent of conducting a transaction in fiat—while potentially enabling smart contract applications.

Although many central banks are developing their own blockchain infrastructure for their CBDC project, several off-the-shelf solutions are currently being considered, including Ethereum, R3 Corda, Quorum, Hyperledger Fabric, and Elements. The realistic prospect of multiple CBDCs has also spawned Cypherium, an enterprise-ready blockchain solution that enables instant transaction settlement, incredibly low fees, and perhaps most importantly, provides a framework that facilitates the interoperability of different CBDCs.

The Potential for CBDC

If you have ever had the misfortune of needing to remit money to a second or third world country, then odds are you are also well aware of the costs involved in doing so.

According to World Bank Group, the average global remittance cost is 6.67% of the transaction amount, but this can range from as high as 8.71% to Sub-Saharan Africa, to as low as 4.92% to South Asia. This is due to inefficient settlement technology and crime prevention, which in combination with regulations and policies, make remittance an expensive endeavor—particularly for smaller transactions.

CBDCs, on the other hand, could be settled almost instantly across borders by avoiding the need for clearinghouses and intermediaries, while cutting fees down to a minimum. Since they may be based on a blockchain ledger, it would also help cut down crime and money laundering, since a record of the transfer would be stored on an immutable database.

But CBDCs also more than just faster, cheaper alternatives to traditional paper money and coinage. They also provide banks with much more control over the money supply, potentially reducing the need for measures like quantitative easing and interest rate adjustments, as counterfeiting becomes all but impossible and inflation can be more easily managed.

Nonetheless, as central banks continue to explore and pilot CBDCs, it will become increasingly apparent whether they can deliver economic growth and potentially improve the velocity of money.