Aave Horizon's Institutional Test: Can Lending Protocols Win Without Retail Leverage?

Institutional DeFi has a simple question to answer this year: if you strip out retail leverage, can lending protocols still scale into real businesses? Aave’s Horizon market is the cleanest test bed we have right now.

Horizon is designed for tokenized treasuries, credit, and other real world assets with whitelisted access. That means less degen reflex and more cash management logic. The upside is sturdier collateral and predictable yield. The catch is demand. Without retail chasing points and perps, who is borrowing on the other side, and at what rates?

This piece gets practical. How Horizon works, what to monitor, the trade-offs you’ll face, and a step-by-step way to approach it if you are an allocator or a protocol treasury.

| Aspect | What to Know |

|---|---|

| Market size now | Aave Horizon’s RWA market holds roughly $540M in total assets with about $163M borrowed, per independent reporting The Defiant. |

| Growth context | Aave Labs previously highlighted over $450M net deposits and ~$135M borrowing as Horizon scaled, positioning it as the largest RWA lending venue Aave blog (Aave Labs). |

| Collateral types | Tokenized Treasuries and credit exposures, plus compliant security tokens like mGLOBAL that keep exposure to an offchain loan strategy while enabling USDC borrowing The Block. |

| Target users | Funds, DAOs, corporates, and market makers with KYC access seeking cash efficiency, yield stacking, or basis trades without taking protocol-native volatility. |

| Access model | Whitelisted pools with parameter controls. Supply and borrow caps can tighten or expand quickly as risk teams tune the market LlamaRisk. |

| Rate dynamics | Utilization driven. With fewer retail loops, borrowing costs hinge on treasury yields, credit spreads, and how aggressively funds want stablecoin lines. |

| Key risks | Liquidity windows, cap changes, oracle and legal plumbing, and concentration in a handful of issuers. Traditional smart contract risk still applies. |

Core Concepts: How Aave Horizon actually works

Horizon is a gated segment of Aave tailored for tokenized real world assets. Instead of volatile crypto collateral, you are mostly looking at tokenized T-bill funds, short duration credit, and compliant security tokens that represent offchain loan portfolios. The idea is familiar: deposit collateral, borrow stablecoins. The difference is the underlying cash flows and the governance stack that keeps them within policy.

Supply side is typically funds and treasuries parking tokenized cash equivalents to harvest base yield plus protocol incentives if available. Borrow side is more selective. Without a mass of retail looping for airdrops, borrowing demand tends to come from market makers, basis traders, and funds financing strategies elsewhere while keeping exposure to their RWA yields.

We have fresh proof points. Aave highlighted Horizon passing $450M in net deposits and around $135M in borrow volume as it scaled its RWA lineup Aave blog (Aave Labs). Independent tallies now peg the RWA market around $539.8M in total assets with about $163.5M borrowed, and note the addition of VanEck’s treasury exposure onchain The Defiant.

On the product side, Midas launched the security token mGLOBAL on Horizon. Holders can post mGLOBAL and borrow USDC while keeping exposure to Fasanara Capital’s Global Diversified Alternative Debt strategy. The Block reports Fasanara manages about $6B and Midas has issued over $2B in assets with $43M distributed in yield to date The Block. That is the kind of institutional rail Horizon is courting.

Glossary: what the docs assume you know

- RWA: Real world asset, like tokenized Treasuries or loan portfolios that live onchain as compliant tokens.

- Whitelisting: KYC or eligibility checks that gate who can deposit or borrow in a given pool.

- Supply cap: A governance set maximum on how much of a token can be deposited to limit concentration risk.

- Borrow cap: An upper limit on how much of a given asset can be borrowed to control utilization and stress scenarios.

- Oracle: The price or NAV feed used to value collateral and calculate health factors.

- Concentration risk: Exposure piling up in a single issuer or asset so that one event hits the whole market.

Step-by-Step Playbook

- Define the job to be done. Is this cash management with optional liquidity, financing for a basis trade, or borrowing against RWA exposure to avoid selling it?

- Map your eligibility. Confirm whitelisting, custody support, and whether your entity can hold each tokenized asset under policy.

- Underwrite the collateral. Read the fund docs, NAV calculation, redemption windows, and legal wrappers. Identify who sits between you and the offchain cash.

- Size against caps. Check supply and borrow caps, plus historical parameter changes. LlamaRisk’s updates show multiple June 2026 adjustments as the market scaled LlamaRisk.

- Model utilization and rates. Simulate how your borrow APR moves as utilization shifts, and what happens if caps change before you draw or repay.

- Build exit paths. Plan for redemptions. For tokenized Treasuries, note cutoffs and T+ settlement. For credit tokens, assume slower liquidity and test stress exits.

- Run a canary line. Start small. Exercise the full loop: deposit, borrow, repay, redeem. Verify onchain accounting matches your back office.

- Set live monitoring. Track health factors, oracle updates, governance proposals, and cap changes. Assign a human owner to every open position.

What changes when retail leverage is sidelined?

Retail loops juice utilization. Remove them and you get a truer read on institutional demand. On Horizon, that demand revolves around three patterns.

First, collateral keepers. Funds park tokenized T-bills to pick up baseline yield and keep optionality to borrow USDC for short windows when an opportunity appears. They do not want to spend that option unless the spread is obvious.

Second, strategy financers. Market makers and credit funds borrow stablecoins against their RWA book to finance external trades, pay for hedges, or manage liquidity across venues. These are measured draws, usually time bound.

Third, structured users. With security tokens like mGLOBAL, holders keep exposure to an offchain alternative credit strategy while tapping USDC for working capital or additional positioning. This looks more like collateralized credit than speculative looping The Block.

The result is calmer, but also patchier, utilization. Borrow rates will not levitate just because yields are up. They move when desks see a trade. That is why governance keeps tuning caps and parameters as supply arrives. LlamaRisk’s June to early July 2026 log lists multiple supply and borrow cap changes across assets, a sign the market is actively stewarded rather than left on autopilot LlamaRisk.

Where Aave Horizon fits vs other RWA lenders

If you are choosing rails, the question is not which protocol wins in abstract. It is which market mechanics fit your mandate and timing. Below is a quick map at the level that matters for investment committees.

| Platform | Access model | Collateral and borrowers | Rate discovery | Liquidity profile | Primary risk focus |

|---|---|---|---|---|---|

| Aave Horizon | Whitelisted pool-based lending with supply and borrow caps | Tokenized Treasuries and credit; overcollateralized borrowing by eligible entities | Utilization curves within caps | Onchain withdrawals subject to asset redemption windows | Parameter changes, oracle feeds, collateral concentration |

| Maple | Permissioned lending pools run by pool delegates | Underwriting of KYC borrowers, often less than fully collateralized | Pool terms set by delegates, borrower negotiations | Pool-specific with lockups and waterfall rules | Counterparty default and recovery |

| Centrifuge | Asset-backed pools bridging receivables onchain | Offchain assets tokenized into tranches; investors select risk tiers | Tranche yields and pool mandates | Dependent on asset cash flows and redemption terms | Asset performance and servicing |

| Ondo | Tokenized funds and credit exposures | T-bill tokens and other RWA instruments usable across DeFi | Fund yields plus venue-specific borrowing terms | Fund redemption windows and venue liquidity | Fund operations and integration risk |

Horizon’s differentiator is composable overcollateralized borrowing against conservative assets in an Aave-native framework. If your risk policy prefers rails with transparent parameters and onchain liquidation logic, it is a natural starting point. If you need true credit underwriting and are paid to take borrower risk, Maple or Centrifuge-type structures may map better.

Pro tip: watch Horizon caps like a hawk. A full supply cap means your allocation will queue. A shrinking borrow cap can strand a basis trade. Subscribe to risk updates and set alerts on relevant governance threads.

Scenarios to model before you wire funds

Even in a calmer market, you want to rehearse the messy edge cases. Here are three to run in a spreadsheet and a staging wallet.

Rising rates compress the wedge. If 3-month bills tick up 50 bps and borrow demand slows, the incremental spread from borrowing against T-bills can vanish. Build rate sensitivity bands for your strategy. Assume you only draw when the wedge clears fees by a safety margin you commit to in advance.

Cap shock. Governance tightens a borrow cap after your desk pencils a trade but before you draw. What is your plan B? Can you split across venues without violating concentration limits? LlamaRisk’s June 2026 activity shows parameter changes are part of normal operations at current scale LlamaRisk.

Asset specific stress. Your collateral is a security token tied to an offchain credit strategy. A redemption delay or valuation dispute hits at the same time you would like to rotate. What is your liquidity backstop and who signs the waiver internally to hold past policy if needed?

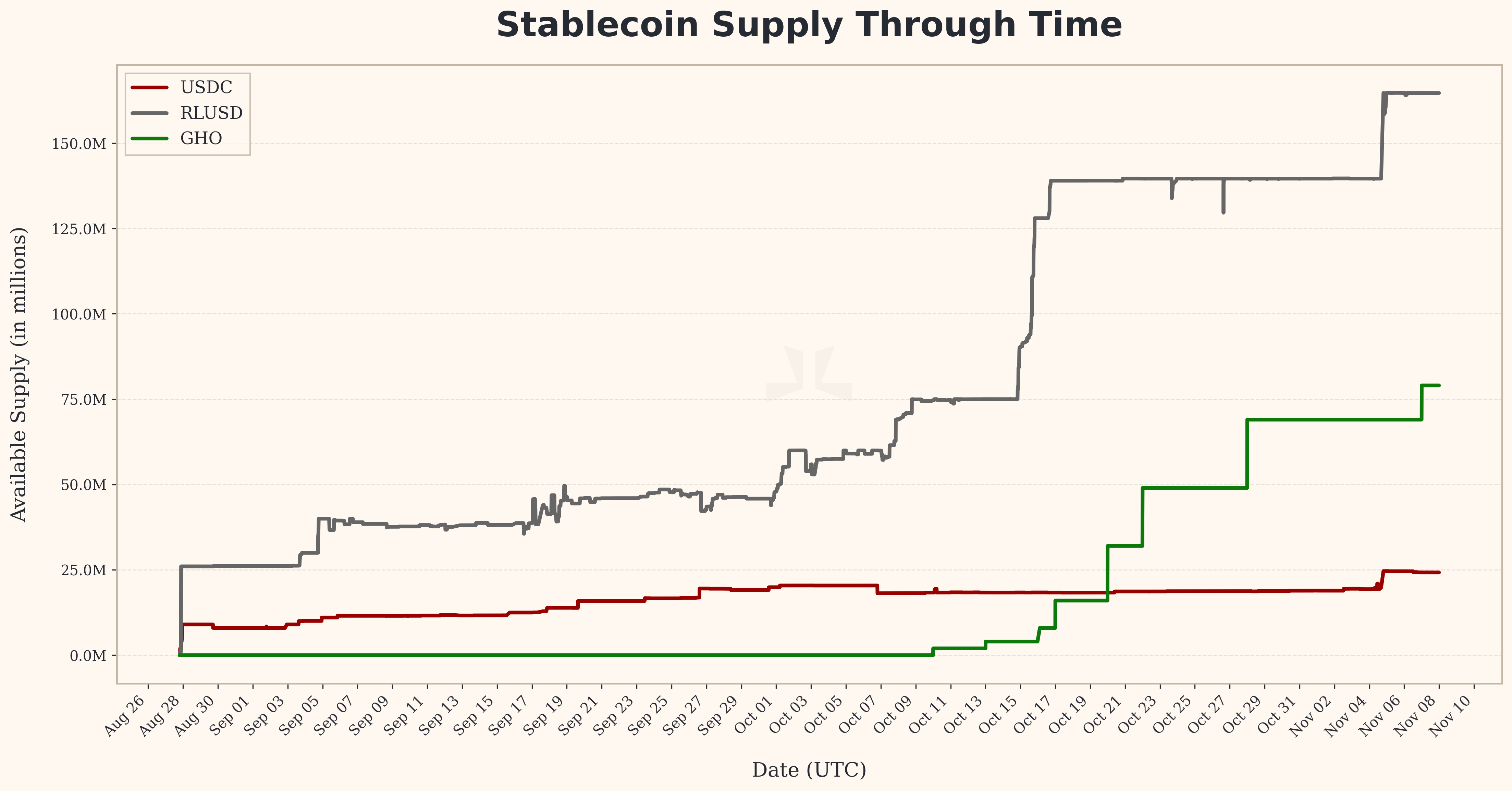

Stablecoin Supply Through Time on Aave Horizon (USDC, RLUSD, GHO) — shows how institutional RWA borrowing has drawn unified stablecoin liquidity onto Horizon and why supply composition matters for retail vs institutional-driven leverage. — Source: LlamaRisk (Aave governance)

Pitfalls & Red Flags

- Ignoring redemption calendars. Tokenized Treasuries settle on schedules. Miss a cutoff and your cash shows up days later than you planned.

- Overlooking cap dynamics. Supply and borrow caps can change quickly, as seen in June 2026 risk updates. Treat caps as active, not static.

- Concentration creep. One issuer looks safest until everyone piles in. Track exposure by issuer and by oracle source.

- Oracles you never tested. NAV updates and price feeds need monitoring. What happens to your health factor on a stale or delayed update?

- Legal wrappers on autopilot. Your entity must be eligible to hold each token. Do not assume cross-venue transferability without new KYC.

- Assuming borrow demand. Without retail loops, utilization comes in waves. Do not size a strategy on the assumption that liquidity will be there on your timetable.

If you want ongoing context with fewer buzzwords, we cover these shifts and the weekly risk chatter at Crypto Daily.

Frequently Asked Questions

Who is actually borrowing on Horizon if not retail?

Primarily market makers, basis traders, and funds financing specific trades or operations for short windows. Some holders of security tokens like mGLOBAL borrow USDC while keeping exposure to their offchain credit strategy, which is more like collateralized financing than speculative looping The Block.

How big is the market today and is it growing?

Independent tracking shows around $539.8M in total assets with about $163.5M borrowed in Horizon’s RWA market, and coverage notes the addition of a VanEck treasury fund onchain The Defiant. Aave earlier cited over $450M in net deposits and ~$135M borrowed as it scaled up Aave blog (Aave Labs).

What is special about mGLOBAL on Horizon?

mGLOBAL is a security token issued by Midas that tracks Fasanara Capital’s diversified alternative debt strategy. On Horizon, holders can post it as collateral and borrow USDC while maintaining exposure to that offchain portfolio. The Block reports Fasanara manages around $6B, with Midas issuing over $2B in assets and distributing $43M in yield so far The Block.

What risks feel different from traditional Aave markets?

Aside from smart contract risk, you need to underwrite legal wrappers, redemption timelines, and NAV oracles. Governance controlled supply and borrow caps are also active levers. LlamaRisk’s June to early July 2026 notes show frequent cap adjustments as the market scaled LlamaRisk.

Can Horizon succeed without retail leverage?

It can, but the curve looks different. Growth depends on onboarding more collateral types, reliable oracles, and institutional use cases that genuinely need short term USDC lines. The recent mGLOBAL launch and the inclusion of tokenized treasury funds suggest that pipeline is real, even if borrowing demand is episodic.

How should a fund size a first position?

Treat it like a pilot. Start with a canary line sized below your smallest redemption bucket. Test deposit, borrow, repay, and redeem end to end. Only scale once operations, legal, and reporting are all green.

Where do I monitor changes that could impact my position?

Track Aave governance for parameter updates, LlamaRisk posts for cap changes, asset issuer dashboards for NAV and redemption windows, and venue analytics for utilization and rates. Set notifications, not bookmarks.

Disclaimer: This article is provided for informational purposes only. It is not offered or intended to be used as legal, tax, investment, financial, or other advice.

Related Stories