Crypto Market Recap Q3, 2023

Crypto experienced a further decline in Q3, 2023. During the summer, there was a gradual cooling of the crypto market, with most assets losing value throughout the quarter. This decline was primarily attributed to difficulties in July. Notably, there was a significant decrease in trader interest, as evidenced by reduced trading volumes and volatility. Even high-profile news failed to stimulate the market and initiate a new trend.

The decrease in interest is indicative of one of the stages in market cycles, suggesting a possible transition toward the final stage of a bear market.

Key Takeaways

-

Markets are red, but it's not as bad as it could be

-

The SEC continues resisting crypto ETFs

-

Friend.tech brings SocialFi back on wave

-

Telegram bots make on-chain trading simple

-

New point of growth for DeFi

-

Crypto fundraising keeps stagnating

-

On-chain picture remains optimistic

Market Review

The performance of the top-100 cryptocurrencies in Q3 was disappointing. Most coins traded in the red, but there was no clear trend. The heatmap resembles a Christmas tree with a mix of green and red colors. Some coins demonstrated exceptional performance during this period, while others gradually declined.

Data source: CryptoRank.io (1.10.2023)

Bitcoin and Ethereum closed the quarter with a nearly 10% price loss, and many other altcoins also experienced declines. Notably, several blockchain tokens, including MATIC, AVAX, ATOM, and ARB, performed significantly worse than ETH.

There were a few projects that had a successful quarter. One notable project is Solana, which experienced a significant drop in performance after the FTX incident. Despite the fear, uncertainty, and doubt (FUD), it managed to end the quarter with a 27% price increase. TON coin was an unexpected addition to the top-10 cryptocurrencies for a short period of time. It experienced a notable 47% price increase following the news of the Telegram app's web3 integrations.

Data source: CryptoRank.io

The list of gainers includes various projects, but there is still no trend or narrative that would drive the entire industry, similar to DeFi in 2020-2021, GameFi in 2021, or even AI in early 2023. Even new SocialFi DApps, which we cover in this article, were unable to drive the industry.

As for Bitcoin, this quarter has been quite depressing. Bulls have been unable to push its price past $28,000 since it fell below that level in mid-August. Even very positive news about Grayscale's victory in court was not enough to push it higher.

Data source: CryptoRank.io

However, there are some positive factors. October is often the best month for cryptocurrencies, and the early days of it prove this once again. The fourth quarter is also a decent period for financial markets and cryptocurrencies, and many traders expect optimism to dominate the market.

Since the beginning of 2023, trading volumes on exchanges have continued to decline. Along with the decline in volumes, there has been a decrease in volatility and, as a result, profitability. Many assets have been trading within a narrow range for an extended period, which has reduced the interest of market participants in trading.

Data source: CryptoRank.io

News and Narratives

We have covered the key events of July and August in our monthly recaps, which you can find here. However, September has brought us new stories that have influenced the markets significantly. Let's dive into them:

The SEC keeps postponing crypto ETFs

One of the hottest topics in the latter half of the year is the introduction of Bitcoin and Ethereum ETFs. The market eagerly awaits the moment when the SEC will change its position and approve the first spot ETF. However, all we are seeing now are applications being postponed.

Bitcoin ETFs were the first to generate interest, but later Ethereum ETFs also became involved. It is important to note that we are referring to spot instruments, while futures ETFs are already being traded in the U.S. and are still struggling.

The consequences of an increase in such instruments are not yet clear. Currently, the market does not have a unified stance on whether companies like BlackRock have purchased Bitcoins or not.

New narrative: SocialFi

The launch of the Base blockchain was truly remarkable. We have already provided detailed coverage of it in our previous recaps. Now, our focus shifts to the most intriguing application on Base, Friend.Tech.

Unfortunately, the majority of activity on friend.tech consists of snipers and traders. Currently, this app is primarily used for earning, such as trading keys or farming airdrop points, and much less for socializing.

Friend.Tech initiated the trend of social apps, which was then followed by fork clones on Arbitrum, Avalanche, and other blockchains. While these clones make the concept more convenient, they do not address the underlying issue: for most users, they are simply a means of making money in a frictionless market.

Telegram Bots Are New Trading Meta

It’s been more accessible than ever to snipe tokens and NFTs. The introduction of Telegram bots for crypto has made working with various DApps more convenient. Unibot was the pioneer in this industry, making trading through the Telegram interface possible. As a result, developers seized the opportunity to create similar applications and earn money through commissions and token sales.

However, the concept is still in its early stages and not flawless. Some projects have been vulnerable to exploits, and others have experienced failed launches. Nevertheless, users have embraced the Real Yield concept, which allows token stakers to receive a portion of trading commissions without the risks associated with liquidity pools.

The Hope for DeFi

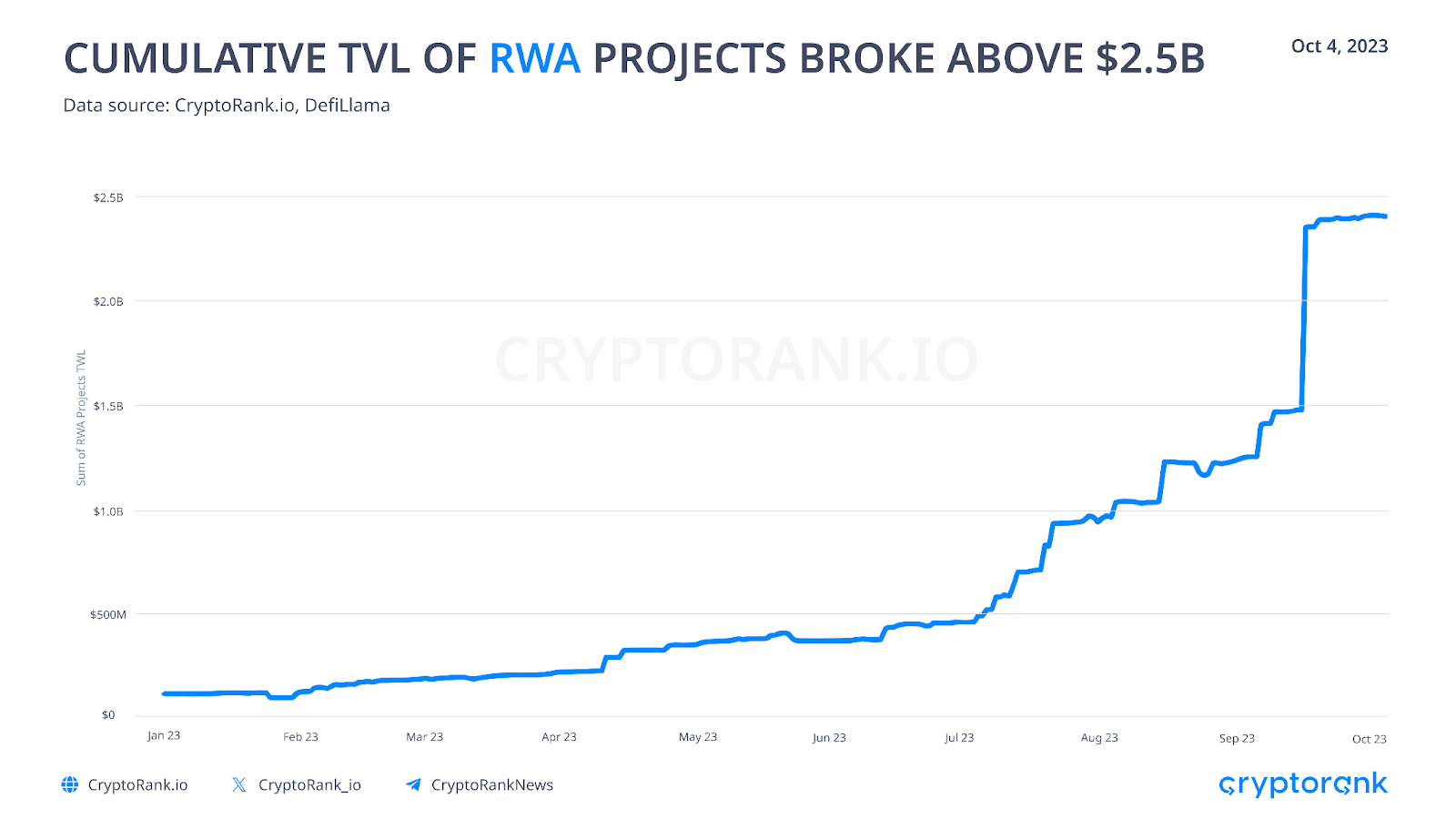

Although decentralized finance (DeFi) has experienced a long decline, new trends are giving us hope for a potential revival. In the first half of the year, Liquid Staking projects demonstrated significant growth, becoming the dominant force in DeFi. Currently, Liquid Staking continues to attract user interest, but Real World Asset projects (RWA) have shown even greater growth in Q3.

RWA is a fast-growing category, although still relatively small. Asset tokenization is not a new trend, but it has gained renewed interest due to declining returns and high risks associated with traditional crypto instruments. Protocol Maker is leading the way by investing a significant portion of its revenues in stable cash flow assets like Treasuries and other securities. Other noteworthy projects in this space include Frax, Canto, and others.

Despite the growth of RWA, the DeFi sector is experiencing stagnation. Ethereum remains the dominant blockchain in terms of Total Value Locked (TVL), with its market share remaining around 70%. Interest in Layer 2 blockchains has slightly decreased, resulting in a slower growth in TVL. This quarter, there may be a shift in TVL from leading Layer 2 blockchains like Arbitrum, Optimism, and zkSync Era to Base, StarkNet, and Linea.

Other blockchains, such as Solana, were also able to demonstrate growth in key indicators during the recovery of coin prices. However, it is still too early to declare a clear trend in DeFi. The crypto market, and decentralized finance in particular, suffers from a lack of liquidity.

Among the protocols, Spark and Binance's ETH staking service showed the largest growth of TVL in the quarter.

Trading volumes on decentralized exchanges are also continuing to decline. The third quarter witnessed a significant decrease, with trading volume on most exchanges dropping by over 30%. The exception to this trend is Maverick Protocol, which, despite being launched relatively recently, experienced significant growth.

Data source: CryptoRank.io

Token Sales and Fundraising

Token sales are currently going through a challenging period. The decrease in trading activity has had a significant impact on token sales. As expected, raised amounts during the summer months were at a very low level. Despite the substantial increase in raises in September compared to August, it is difficult to observe any positive change: the yield of token sales remains low.

Data source: CryptoRank.io

However, there are still robust Launchpads in the market that continue to launch strong projects. Binance Launchpad, in particular, stands out as a leader and recently had the most profitable IEO (Initial Exchange Offering) of the quarter with Arkham. Despite the market slowdown, Binance Launchpad has already demonstrated multiple successful project launches in 2023. Considering the exchange's scale and influence, we can anticipate more successful launches in the future.

Data source: CryptoRank.io

The performance of IDO (Initial DEX Offering) has shown significant underperformance compared to IEO. Many launches have resulted in unprofitable outcomes for investors, and even some prominent launches have failed to present promising projects. However, there are still some notable leaders in this space, for instance, SophiaVerse and Solidus have recently emerged, offering actual AI solutions, and DexCheck, which is a platform for on-chain trading. It is worth mentioning that both Solidus and DexCheck are backed by the full-stack VC Castrum Capital.

Data source: CryptoRank.io

Currently, only a few projects out of dozens launched each month demonstrate positive returns. This significantly restricts the growth of launchpads and token sales, as they mostly lack users. However, without an influx of new capital into the industry, stable high returns cannot be expected. Ethereum, BNB Chain, Arbitrum, and Polygon ecosystems lead with a huge gap by the number of raised amounts. Meanwhile, the BNB Chain ecosystem leads by the number of launched projects and with their ongoing development of the opBNB blockchain ecosystem, can be expected to continue growing over time.

Data source: CryptoRank.io

Regarding private fundraising in the crypto industry, we can also observe stagnation. Although there was a significant increase in the number of investments in September, the trends remained unchanged throughout the third quarter.

Data source: CryptoRank.io

Notably, Binance Labs was the most active investor in the quarter. This fund invested in 12 projects, with the majority of them being DeFi-related. Following Binance Labs, the venture capital arm of another major exchange, Coinbase, as well as its former CTO Balaji Srinivasan, also made notable investments.

Data source: CryptoRank.io

On-chain Delve

On-chain indicators of blockchains do not reflect the same negative sentiment as some other indicators of the crypto market. The utilization of blockchains continues to grow, albeit with popularity shifting from one blockchain to another.

BNB Chain remains the leader in terms of unique addresses, followed by Polygon and Ethereum. Base has increased the total number of users by 1,277% in just 30 days by the end of September. Another winner of the month is Optimism, with nearly 127% increase. Do note that data on Solana is missing due to difficulties in calculation.

However, Solana was the most popular blockchain in September with almost half a billion transactions. Popular Layer 2 blockchains zkSync Era, Base, and StarkNet also secured strong positions in the top-10.

NFT Trading Volume Continues to Decline

The NFT market is currently in a poor state. While there was some optimism at the beginning of the year, it quickly faded. Currently, NFT trading volumes are similar to those of early 2021, before the NFT boom started.

Ethereum remains the leading blockchain in terms of NFT trading volume. Polygon consistently vies with Solana for the second position, but thus far, no blockchain besides Ethereum has managed to establish itself as a "hub for NFTs".

In the NFT market, there are frequent changes and launches of new projects. While NFTs are a significant part of blockchain culture, they tend to underperform in bear markets compared to many other projects.

The Bottom Line

The third quarter of the year was rather uneventful for the crypto market. The main factors driving the market were the expectations of Bitcoin spot ETF approval and new liquidity inflow into crypto. However, it is still premature to declare the end of the Bear Market.

Despite the decline in investments into crypto, the blockchain industry continues to evolve. Strong narratives are emerging in DeFi and SocialFi, which are likely to become the main trends in the next bull run.

It is challenging to anticipate a complete turnaround while there are significant problems in traditional finance and a looming crisis. The crypto market is interconnected with traditional finance, as many companies rely on external funding. The influx of money from outside remains the primary driver of crypto growth. As the world works to solve its problems, the crypto market has a unique opportunity to focus on building and increasing stability.

Disclaimer: This article is provided for informational purposes only. It is not offered or intended to be used as legal, tax, investment, financial, or other advice.

Related Stories