Solving the “Dead Man’s Crypto Conundrum”: How to Securely Transfer Crypto to Your Heirs

Not everyone thinks about what happens after their death. But, even if we don’t like the thought of leaving this world, we should still make sure that our loved ones, our family and friends, will inherit our assets. It’s pretty easy to include and transfer real estate, stocks, and bonds or the money in a bank account from a will. But, what about cryptocurrency? You can’t simply go to a lawyer’s office and hand over all your private keys. You could, but sharing your private information with anyone – even if you trust them today – opens up a huge security risk for your crypto. On the other hand, if you don’t share your private info with someone else, your heirs can’t and won’t ever get access to your digital assets. This is the “dead man’s crypto conundrum.”

Crypto is designed specifically to prevent any access to it against the owner’s will. There is no central control to call for help and no governmental or other recourse in the case of lost private keys or stolen crypto. So, what is crypto heritage and how can any person bequeath his or her crypto funds without compromising their private information – e.g., account credentials, seed phrases, private keys, etc. – to someone like a tax attorney, custodial service or even the beneficiary themselves?

This article aims to answer all these questions and serve as a detailed guide to prepare for the inevitable. We’ve found many solutions people are using to try to solve this problem, including sharing seed phrases and keys of their popular wallets (i.e. Electrum, Ledger Nano, Trezor) to safety deposit boxes. Or setting up “digital wills” on services like Pickled Assets or BoxTomorrow. Or even paying for “technical executors.” All of these options have various pros and cons including cost, convenience, and security. But, despite our initial skepticism, we think we’ve found one new solution that could solve this conundrum – called Keevo. If you want to learn more about all these options and how this new and unique hardware wallet could work out for our future, keep reading.

How much “dead crypto” is out there?

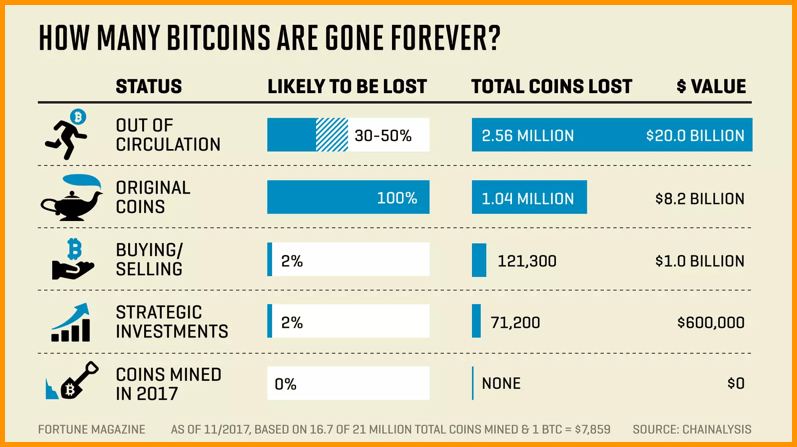

According to various estimates, the total amount of lost or “dead” Bitcoins is approaching 4 million (out of the 21 million maximum cap and 17.8 million already mined as of today). That’s over 20% of the bitcoin in circulation or more than $40 billion in value at current exchange rates. We don’t know yet how much of this “dead crypto” or lost supply belongs to deceased people, and how much is lost simply due to carelessness such as forgotten passwords, computers in landfills, discarded hard drives or lost seed phrases, but we can find all too many cases where relatives are attempting to recover the lost crypto of tech-savvy relatives who have died – all in vain.

For example, one man’s brother died, and he didn't know how to restore access to his wallet, asking questions on forums. Or a similar story where a fiancé died and left his fiancée as the executor of his estate. She was told he had Bitcoins, but she had no idea how to recover them. Or, relatives whose financial sleuthing discovered numerous transactions indicating their deceased loved one owned a small fortune in a Coinbase account.

Sources: coinsutra.com, Chainanalysis

Sometimes crypto investors can die with tremendous balances in their wallets. Matthew Mallon, a banking heir, died at the age of 54 with more than $500,000 worth of XRP stored in his unrecoverable wallets. He left a will, of course, and his family was able to inherit his cash money, real estate, and stocks – but not his crypto. There's a slight possibility that XRP, being a centralized cryptocurrency, can be returned to Mallon’s family by the Ripple Foundation and other members of the network, but it seems highly unlikely.

Speaking of large capital, what about the inactive Satoshi blocks? Approximately 4.5% or 1,000,000 BTC (and various forked coins, such as BCH or BTG), which are currently worth $10.3 billion are all lost. We don’t know the identity of Satoshi Nakamoto, we don’t even know if it was a single person or a group of people. But if it was one person holding the access to these genesis coins and he or she is dead, they could have taken their private keys – and their bitcoin – with them to their grave, as the Satoshi coins have not had a single transfer since they were mined 10 years ago.

Crypto is still in its early stages, so there aren’t any established practices for intermediaries. And, many of these solutions come with their own perils. For example, Gerald William Cotten, the CEO of QuadrigaCX, Canada’s largest crypto exchange, died unexpectedly in December 2018 from Crohn’s disease after travelling to India. He was apparently the only one in possession of the private keys to the cold storage containing more than $190 million worth of crypto funds. These were the funds belonging to more than 115,000 customers. Cotten’s laptop, email addresses, and messaging system were encrypted, making it impossible to find even the traces of the funds. The later investigation reported that QuadrigaX presumably never fully invested the funds entrusted to it, and Cotten used these funds to trade on other exchanges. (Another lesson telling us that your money isn’t truly safe or even yours when it leaves your wallet and it’s stored on a custodial solution like many online exchanges).

As we can see, it’s currently near impossible to inherit crypto funds if the deceased owner didn’t share their private keys or personal wallet information with someone before they die. And, many people don’t or shouldn’t do this as it goes against the very premise and privacy concept of cryptocurrency ownership.

So, let’s take a deeper look at the problem and learn from how traditional institutions are solving this beneficiary transfer and inheritance with fiat currency and other regulated assets.

Inheritance - the traditional way

First of all, before transferring the rights for any property, a person’s death must be validated. Usually, this is done with a government-issued death certificate. Each government prescribes its own procedures necessary to legally produce and authenticate this document, but in general, before issuing a death certificate, the authorities require a certificate from a licensed physician or coroner which declares the cause of death and validates the identity of the deceased. The death certificate is necessary for arranging many things, such as the burial ceremony, and it’s also necessary to present when claiming the inheritance and transferring ownership of assets from the deceased to accounts owned by their heirs.

After that, heirs, or named beneficiaries of the deceased, must be determined in the signed and notarized will for the inheritance process to begin. In most countries and circumstances which typically depend on the size of the inheritance, a will must be submitted to probate. The probate court will then review the will, authorize an executor, and legally transfer assets to the named beneficiaries as outlined in the will. Before the transfer, the executor will settle any of the deceased’s remaining debts, including various tax withholdings by governmental agencies.

Source: theedgemarkets.com

In most cases and before receiving the inheritance, beneficiaries must pay inheritance taxes. As the chart above illustrates, they vary quite a bit by country and state, but the governments of the most developed countries levy taxes of 25-50%. That’s a lot of death taxes. The whole process from beginning to end is supervised by government authorities to exclude the possibility of fraud, but also to make sure that the government gets to collect their taxes. Currently, it doesn’t work this way with cryptocurrencies.

With self-sovereign cryptocurrency, you rely only on yourself

Cryptocurrencies are the total opposite of everything described above with centrally controlled and regulated assets like cash, stocks and bonds, and real estate. With crypto, there’s no need, or desire frankly, for third party intermediaries – governments, banks or other regulated institutions – supervising stored funds and transfers. Every crypto owner has to care about the safety of his/her funds by themselves, and the only time when the funds can be lost is when the owner compromises their private keys. This is both a tremendous power and liberating force, but also a huge responsibility that introduces new complexities and challenges. More specifically, that’s exactly why transferring and inheriting cryptocurrencies is such a problem.

We can break this crypto inheritance problem into two parts:

- First, validating an owner’s death. This one is relatively easy – after all and as per above, we have the government defining that the person is dead and issuing the death certificate.

- The second part of the problem is more serious. How can you transfer control over something you can’t control and that needs to be entirely private? Even if the law or a court decides that everything the deceased person owned should be transferred to a living heir, it can’t simply order and execute the transfer of something they don’t and can’t control.

Wouldn’t storing our private keys at banks, a third party institution, or a trusted person solve this problem? Yes and no. While this might help transfer your crypto to a beneficiary AFTER you die, it might also expose your crypto to loss or theft BEFORE you die. And, unlike other regulated assets, once your crypto is gone… it’s really gone!

Solutions for transferring crypto after you die

So let’s break it down. There are various ways to transfer crypto after the death of the original owner. Each has its own pros and cons:

- Custodial solutions, such as exchange accounts on Coinbase, Binance, or Kraken. These centralized exchanges operate in a manner similar to banks and brokerages, so they can transfer crypto to a beneficiary if they get a court order. In this case, the owner has already given up their privacy and control to a third-party intermediary. While this may be convenient, it can also be incredibly unsafe as we have seen earlier with the QuadrigaCX example and the many other cases of hacks and attacks which have plagued many online exchanges.

- Another way to transfer your crypto to a beneficiary after death is to write down and store the private key or seed phrase of your wallet (i.e. Electrum, Exodus, Mycelium) and tell the beneficiary where that information is stored. If the owner trusts their beneficiary enough to suppose that this information will stay private until their death, then it’s okay. But life being life, trust between humans can change, even among family members. This private information is exposed and if someone gets access to your private keys or seed phrase, all your crypto could be stolen. And again, once your crypto is gone, it’s gone forever.

- Another method of transferring crypto to a beneficiary is by first storing it on a hardware wallet like a Trezor or Ledger, then sharing the private wallet account information – username, passwords and/or seed phrases – with a beneficiary. But again, if this information is compromised or trust between individuals is broken, your crypto could be at risk.

- Another layer of security would be storing your private information and the hardware wallet itself in a bank safety deposit box. And, while a bank may provide a security layer in case of a fallout of trust between the owner and their named beneficiary, it also introduces another party who has potential access to your private keys. When doing so, a bank customer must remember that these safes are also targets for theft and that there are no rules which require banks to compensate customers if their property is stolen or destroyed. Also, it would be near impossible to prove the stolen crypto was even yours in the first place. And, banks are also regulated by governments and other institutions which means that instead of going into the heir’s hands, the private keys can go directly into the hands of institutions if they decide so.

Source: dilbert.com

5.Another common method is entrusting the private keys and hardware wallets to a third party executor named in an owner’s will. Again, this solution requires the user to trust, or at least place their trust and their private information, in the hands of another human being. And, as wills after death become probate court documents, they introduce another layer of government oversight and potential loss of control.

6.You can even consider hiring a separate “technical executor” as, in the case of your heirs not being as technical as you, they might need guidance on retrieving your digital funds. While this might give you some peace of mind, it’s expensive and, again, you are adding one more third-party that has access to your private information.

Based on our research, while looking into how the most popular crypto wallets like Electrum, Exodus, and Mycelium are handling access, or how hardware wallets like Trezor and Ledger can be used for setting up a beneficiary service. And even considering using centralized exchanges like Coinbase, Binance, or Kraken. Still, we weren’t able to find any solution which enables an owner of crypto to transfer their virtual assets to a named beneficiary AFTER their death without first sharing their private information – and entrusting the security of their crypto – with a third party BEFORE their death.

That was... until we came across an ambitious sounding, next-generation hardware wallet called Keevo.

An advanced wallet that solves the conundrum

Keevo is a relatively new wallet but with an impressive team of experienced entrepreneurs, security experts, and developers behind its creation. The Keevo engineers are trying to break the compromise between security and convenience of all the other hardware and software solutions on the market and described above.

Keevo claims to be as secure and private as a Swiss numbered bank account in your pocket… but without the bank!

As we dug into the details of their solution, we discovered that breaking this “dead man’s crypto conundrum” is a core benefit and problem they claimed to have solved. We were intrigued. Very intrigued. So… how are they solving the conundrum?

In addition to a lot of new, state-of-the-art security technology and sleek and simple design is the heart of the Keevo solution: a paperless recovery system built around what they call multi-factor / multi-signature authentication. This system allows users to recover their private keys on any Keevo wallet by entering or signing any three out of four of the following factors:

- The device itself (something you have)

- A strong PIN created by the user (something you know)

- The user’s fingerprint (something unique to you)

- The Keevo Carbon Key, a secondary hardware device with another unique key and encrypted copies of the above keys (something you store)

As the first hardware wallet with 4-Factor Authentication (4FA), Keevo enables users to recover their private keys without having to deal with the hassle of writing down and securely storing a paper seed phrase for recovery. Instead, users can store the Keevo Carbon Key – or for a nominal fee, Keevo will store the Carbon Key for you in one of their enterprise-grade storage facilities – and use this secondary hardware device and fourth factor as a backup solution. That, in and of itself, is pretty cool. But, what we found even more novel and really unique was that users could also name a beneficiary and have them enter their fingerprints and create their own strong PIN which is then encrypted and securely stored on the user’s Carbon Key, too. That’s really cool!

In this way, Keevo’s Carbon Key is a “smart will” that’s totally private and secure but also effective in transferring ownership and control of your crypto to a named heir after you die. The owner never has to share their private keys or account information with anyone, even their beneficiary, before they die. But, AFTER they die, the beneficiary can validate the user’s death with Keevo and receive the user’s Carbon Key which has their encrypted information securely stored in it. Then, with the beneficiary’s own fingerprint and the PIN they created and previously stored on the user’s Carbon Key – along with Keevo’s one-time co-signature to confirm the user’s death– the beneficiary can restore the user’s private keys and access their crypto.

Source: xkcd.com

Keevo’s solution seems very elegant, convenient and secure. It’s strange that nobody came up with this idea before. It seems so simple. But, obviously there’s a lot of technology - and they claim to have filed a patent, too -- behind this. And, as per above and as best we can tell, it’s the only way to transfer your crypto after you die without sharing any private information with anyone beforehand.

Let us know what you think. Do you know of any stories related to crypto inheritance, the “dead man’s crypto conundrum”, and how this problem is being solved? Do you know of any other solutions to safely and privately transfer your crypto after you die without first sharing your private information with another person before you die? Please feel free to share your input and any suggestions on this important topic! Solving this conundrum will only become more and more important as we all get older and the total amount of digital currencies and crypto market value increases as crypto becomes an ever-increasing share of investors’ and consumers’ asset portfolios!