FOMC Minutes Week: Why the S&P 500 Rally Still Depends on Rate-Cut Patience

It’s minutes week. The Fed will open the hood on its June meeting, and stocks will try to figure out if the engine’s still running smooth or starting to ping. If you care about the S&P 500 holding its massive Q2 run, this one matters.

We’ll break down what in the minutes can shake equities, why “patient cuts” beat “fast pivots,” and how jobs, inflation, yields, and the dollar tie together. You’ll get a plain checklist for release day, a sector map for different rate paths, and a read-through for crypto risk.

Quick heads-up on timing: the June 16–17, 2026 FOMC minutes hit on Wednesday, July 8 at 2:00 p.m. Eastern. Mark the clock. That’s straight from the Fed’s calendar Federal Reserve (FOMC calendar).

The S&P 500’s rally still leans on a slow, steady path to rate cuts rather than an urgent pivot. The market wants confirmation that inflation risks are easing enough to trim rates later this year without the Fed signaling fear about growth. Patience keeps the soft-landing story intact; rushing would hint at trouble.

- Minutes timing: Wednesday, July 8, 2 p.m. ET.

- Fed’s June projections lifted the 2026 median policy rate to 3.8%, with inflation risks skewed up Federal Reserve — Summary of Economic Projections (June 17, 2026).

- Q2 was huge: the S&P 500 jumped 14.9%, best since 2020 Reuters.

- Markets lean toward cuts starting in September or October, but with caveats OANDA.

What in these minutes could move stocks this week?

Start with the basics. We’re not getting new dots or fresh data in the minutes, but we are getting context. Who leaned hawkish and why? Did anyone float tolerance for a slower disinflation path? Was there concern about growth stalling?

Because the minutes arrive on Wednesday, July 8 at 2:00 p.m. ET, you’ll see the first move in rates futures and the 2-year yield, then equities react. The key is whether the language implies the bar for cutting is still high, or just high enough to avoid rushing. If the text emphasizes upside inflation risks or discomfort with easing financial conditions, expect a knee-jerk higher in front-end yields and a sideways-to-softer equity tape.

Grab a notepad. The details matter more than headlines. If the minutes show broad agreement to wait for multiple months of cooler inflation before cutting, that’s supportive for a “patient cuts” story. If they show nervousness about growth, rate-cut odds jump fast, but stocks might not love what that implies.

- Language to scan for: “some participants,” “many,” “most,” and “broad agreement.” These are tells for how widespread a view really was.

- Mentions of “financial conditions” easing or tightening.

- Any reference to labor softening beyond expectations.

- Discussion of the balance of risks: inflation vs growth.

- Comments on term premiums and long-end volatility.

Why does the S&P 500 still rely on patient rate cuts?

Equities rallied hard into the end of Q2. The S&P 500 rose 14.9% in the quarter, its best since 2020, which raises the bar for new upside and leaves little room for policy error Reuters. Stocks don’t actually want rapid cuts. Rapid cuts usually mean something’s breaking.

What they want is glide-path confidence. The Fed’s June Summary of Economic Projections pushed the median 2026 policy rate up to 3.8% from 3.4% in March, and 17 of 18 participants said inflation risks were skewed to the upside Federal Reserve — Summary of Economic Projections (June 17, 2026). That’s not a backdrop for an aggressive pivot. It is, however, consistent with a slow set of trims once the committee is comfortable inflation is drifting down while growth holds.

Patience keeps financial conditions from snapping tighter or looser in a single week. Fewer whipsaws mean valuations can rely on earnings, not just rate beta. Said differently: stocks prefer an orderly descent to neutral over a parachute jump into a storm.

Pro tip: If the minutes sound more eager to cut, don’t cheer automatically. Fast cuts often show up when growth risks are biting. That’s not great for cyclicals, small caps, or high-beta tech on a sustained basis.

How are jobs, inflation, and earnings setting the backdrop now?

The labor market has cooled, but it hasn’t cracked. June saw a 57,000 rise in nonfarm payrolls and a 4.2% unemployment rate, per the BLS release on July 2 Bureau of Labor Statistics. That’s a softer print than earlier in the cycle, aligning with a gentle slowdown narrative.

Inflation remains the swing factor. The Fed’s June projections flagged upside inflation risks for 2026, with 17 of 18 FOMC participants seeing the risks skewed that way Federal Reserve — Summary of Economic Projections (June 17, 2026). Translation: they’ll want convincing, repeated progress before they cut.

Corporate earnings season will set the tone right after the minutes. If companies talk about stable demand, decent margins, and manageable wage pressures, that backs a “patient cuts” path. If guidance gets wobbly, the market could beg for faster relief, which is not the message the Fed has been sending.

![]()

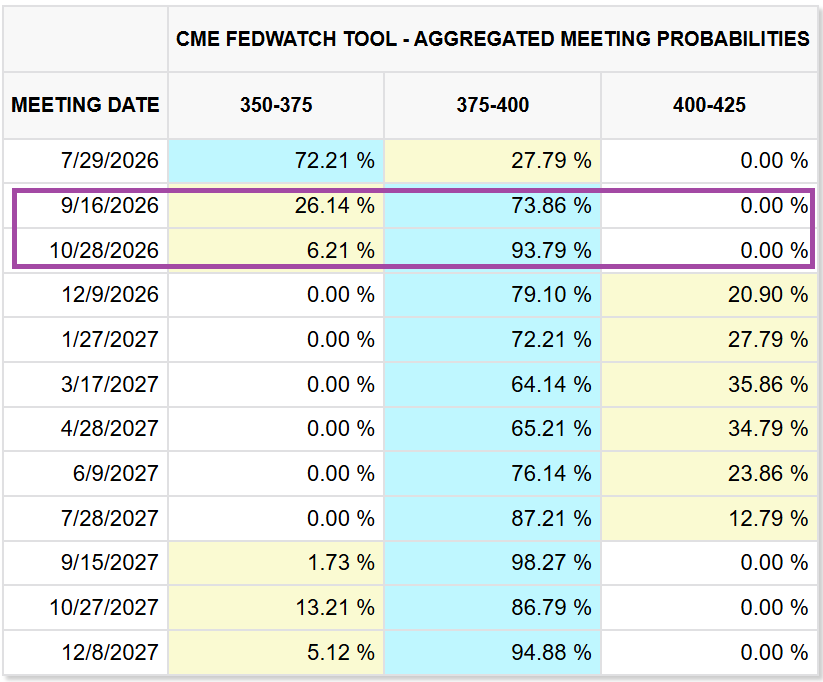

What are markets pricing for September and October?

Heading into July, market-implied probabilities had been leaning toward a first 25 bp move in September and another in October, with a snapshot around late June showing roughly 73.9% odds for September and 93.8% for October, respectively OANDA. Treat these as moving targets, not gospel. Each inflation print, each labor update, and yes, these minutes can nudge that curve.

What matters for stocks is not just the first cut, but the cadence after it. A slow cut every meeting or two with firm data is bullish enough for quality tech and large-cap growth. A faster sequence because growth is sliding is a different story.

Watch the 2-year Treasury. If it pops higher on hawkish minutes and stays there, equities may chop as multiples adjust. If it dips but credit spreads widen at the same time, that’s not the rally you want.

Which sectors hold up under different cut paths?

No crystal ball here, just playbooks. Think in scenarios and keep a short leash.

| Scenario | Policy vibe | Equity tilt that often benefits | Key watchouts |

|---|---|---|---|

| Baseline: patient cuts start late Q3 | Inflation easing, growth steady | Quality tech, megacap growth, healthcare, staples | Multiple drift if long-end yields back up; earnings delivery needed |

| Faster cuts: front-loaded in 2H | Growth scare brewing | Long-duration assets bounce first; cyclicals fade on weaker demand | Credit spreads widening; earnings downgrades risk |

| Slower path: cuts slip to late year/into 2027 | Sticky inflation or upside surprise | Energy, value pockets, cash-generative industrials | Higher real yields pressure high-multiple names |

Remember, sequences matter. A couple of patient trims with calm credit and contained inflation beats a dramatic slash that spooks credit and the dollar in one go.

Where do bonds, dollar, and crypto fit into this picture?

For bonds, the front end keys off the minutes. Hawkish tone? 2-year yields pop, curve may flatten. Dovish tone on growth? Front end drops, but if that dovishness is growth fear, long-end duration can rally while cyclicals underperform.

The dollar usually follows rate differentials and risk appetite. A firmer path to patient cuts with upside inflation vigilance tends to keep the dollar supported. A growth scare that drags yields down fast can weaken the dollar, though it might also lift volatility across assets.

Crypto sits between liquidity and risk appetite. A patient-cut path that avoids a hard landing is generally constructive for risk-taking without the “panic cut” signal. If the minutes push back on near-term cuts while inflation risks remain top of mind, expect crypto to take its cues from broader liquidity expectations and the dollar’s path rather than a single headline.

CME FedWatch aggregated meeting probabilities (snapshot as of June 26, 2026) — shows markets pricing a ~73.9% chance of a Sept. 16, 2026 hike and ~93.8% for Oct. 28, 2026, underlining why equity rallies (S&P 500) hinge on the timing of rate‑cut expectations. — Source: OANDA

How to prepare for minutes day and the week after?

Have a simple game plan. The first move isn’t always the right one. Let the text settle, then the rates market, then equities.

- Set alerts: 1:55 p.m. ET and 2:00 p.m. ET for the drop.

- Read the balance-of-risks language twice before trading the takeaway.

- Track the 2-year yield, belly of the curve, and credit spreads in real time.

- Cross-check with the June SEP: 3.8% 2026 median and upside inflation risks kept the bar high Federal Reserve — Summary of Economic Projections (June 17, 2026).

- Keep an eye on labor data follow-through. June NFP +57,000 and 4.2% unemployment signal cooling, not collapse Bureau of Labor Statistics.

Common Mistakes

- Trading the headline, not the nuance. The first sentence rarely captures the committee’s center of gravity. Read the risk-balance paragraphs before moving size.

- Assuming fast cuts are bullish for stocks. Quick relief often rides with growth fear. Cyclicals and small caps don’t love recessions.

- Ignoring the 2-year yield. This is the equity multiple thermostat. Large jumps can compress valuations even if the long end is calm.

- Forgetting positioning. After a 14.9% Q2, marginal sellers show up faster on hawkish surprises Reuters.

- Reading minutes without the SEP in mind. The 3.8% 2026 median and skewed inflation risks frame all the prose Federal Reserve — Summary of Economic Projections (June 17, 2026).

If you want a daily pulse on how macro flows feed into digital assets, we cover it in plain English at Crypto Daily.

Frequently Asked Questions

Do the minutes change the dots or official rate projections?

No. The minutes only explain the discussion behind the June decision and projections. They can shift probabilities by revealing how firm or divided the committee was, but the dots themselves don’t move.

Could the minutes push markets to price out a September cut?

Yes, if the text leans heavily on upside inflation risks and comfort with the current stance. A clear “wait for more evidence” tone can nudge odds lower for September and backload expectations into October or later OANDA.

What if the minutes hint at worsening growth?

Then front-end yields likely drop and cut odds jump. Equities might rally initially on easier policy hopes, but cyclicals and credit could struggle if it smells like a real slowdown. That’s not the rally you want carrying into year-end.

How much does the labor print matter next to the minutes?

They’re complementary. June payrolls of +57,000 with 4.2% unemployment suggest cooling, which supports patience rather than urgency Bureau of Labor Statistics. If the minutes sound hawkish despite that, the market will re-check the inflation path.

Is the Q2 surge a sign of durability or fragility?

Both. A 14.9% quarterly jump proves momentum, but it also concentrates risk around policy surprises and earnings delivery. The higher you climb, the more sensitive you are to small shifts in rate expectations Reuters.

What should crypto traders watch specifically?

Watch the 2-year yield, the dollar index, and credit spreads the hour after release. A patient-cut tone with stable credit is better for risk; a “fast cuts for growth fear” tone can lift duration but raise cross-asset volatility.

Is there a single line in the minutes that matters most?

Not really. But the balance-of-risks paragraph comes close. If it reads like “inflation risks still to the upside, growth resilient,” that’s patient cuts. If it flips toward growth concern, you’ll see it first in rates, then in equities.

Disclaimer: This article is provided for informational purposes only. It is not offered or intended to be used as legal, tax, investment, financial, or other advice.

Related Stories